JudeEsq

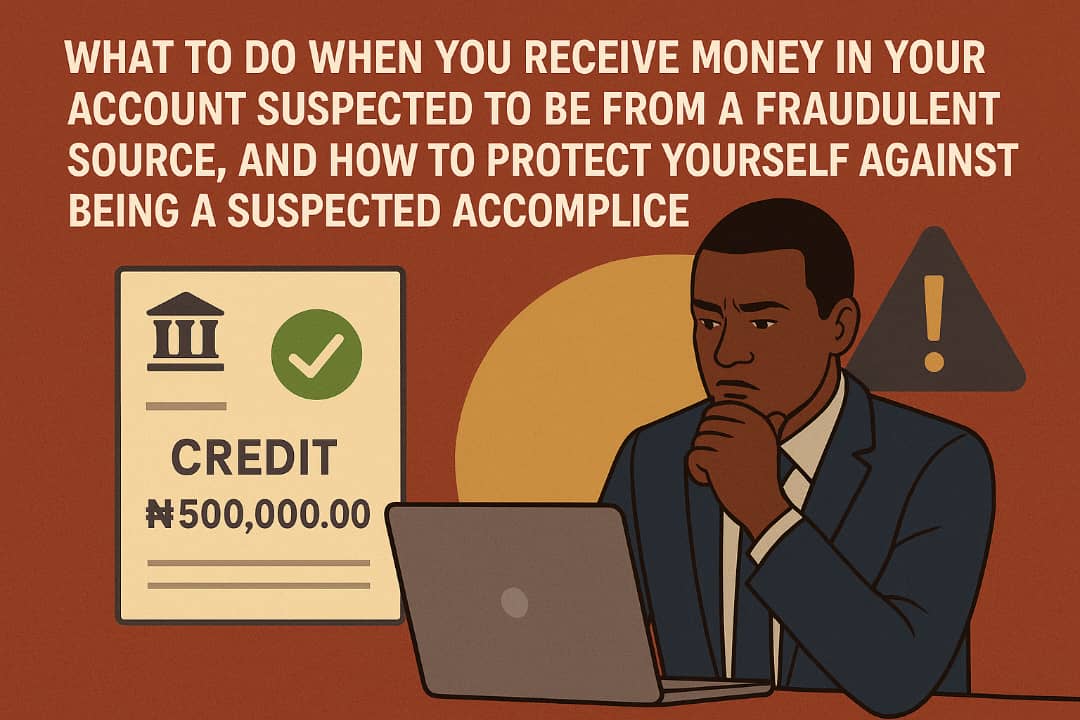

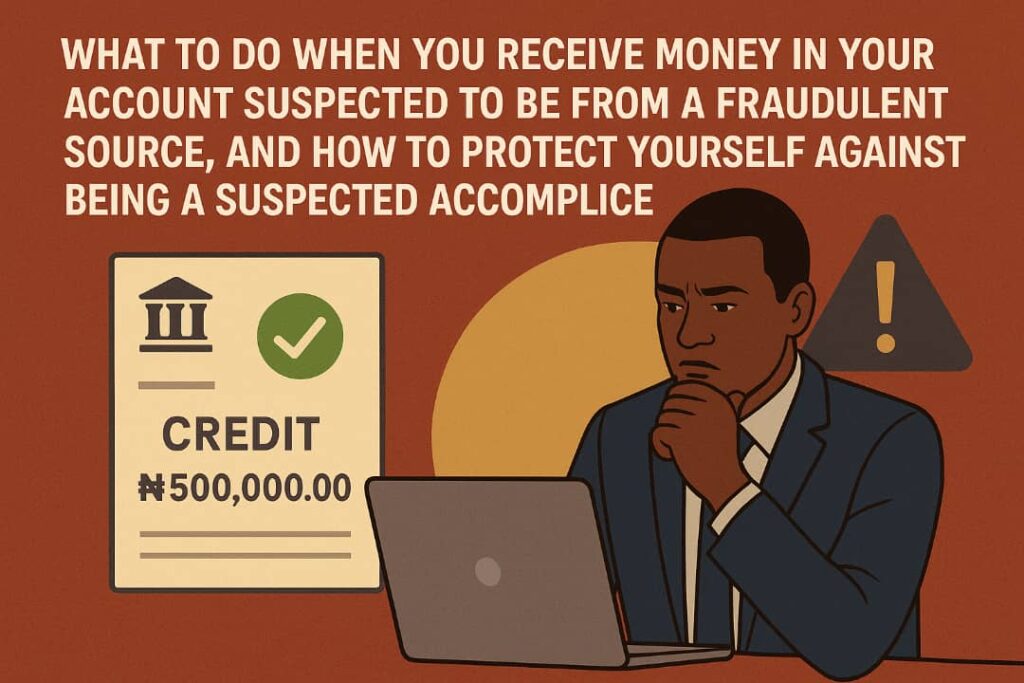

Finding an unexpected credit in your bank account is jarring. Your first instinct may be relief or curiosity. The correct response is caution. Under Nigerian law, knowingly keeping or dealing with money that is the fruit of a crime can attract serious criminal liability. This short guide tells you, step by step, what to do the moment you notice the credit, how to protect yourself from being suspected of wrongdoing, and how to document your actions so you can explain yourself if investigators come calling.

Why you must act quickly and carefully

There are two separate legal exposures to keep in mind. The first is the criminal law offence of receiving property that belongs to another where you know or reasonably ought to know that the property was stolen. The second is the offence of handling the proceeds of unlawful activity under the money laundering law. Both are grave. You do not need to jump to the conclusion that you committed an offence, but you must behave in a way that shows you had no guilty knowledge and that you tried to correct the situation as soon as you discovered it. For the rule on receiving stolen property, see Section 427 of the Criminal Code Act of Nigeria. For the modern framework that addresses proceeds of crime and suspicious financial activity, see the Money Laundering Prevention and Prohibition Act 2022 and the guidance issued by the national financial intelligence authority.

Immediate steps to take the same day you discover the credit

- Stop using the funds

Do not withdraw, transfer, spend or move the money. Any disposition may be used as evidence that you treated the money as yours. Even returning a part of the funds without following proper channels can complicate your position. - Take screenshots and save records

Capture the bank alert, your online statement showing the incoming credit, the full transaction reference, the sender account name, and any messages or notifications. Record the date and exact time you noticed the credit. - Contact your bank by phone and by writing

Call your bank immediately and tell them that you have an unexplained incoming credit and that you do not consent to using it. Follow up with a short, factual email or secure message through your bank account. Ask the bank to place a hold on the amount pending investigation and to provide written confirmation of the request and any steps they take. Financial institutions are required to investigate suspicious transactions and to report them where appropriate. Public guidance from the central bank of Nigeria and major banks instructs customers to report unexpected credits and to notify the bank immediately. - Do not contact the alleged sender directly unless your bank advises it

Contact between you and an unknown sender can be cited as suspicious conduct. Let the bank or the proper authorities do the tracing. - Notify a lawyer and prepare to preserve evidence

Tell your legal adviser exactly when you discovered the money and what you did. Ask the lawyer to send a short instruction to the bank asking them to preserve logs, video where relevant, and all electronic records related to the payment. A lawyer can also help you draft statements later that are consistent and careful.

How to talk to the bank and to investigators

Be factual, concise and consistent. Offer the following information in writing and keep a copy for your records.

• State that you discovered an unexplained credit on a specific date and time.

• Give the transaction reference, the sender information as shown on your statement, and the amount.

• State that you did not authorise the funds and that you request the bank to investigate and to freeze or return the funds if they are proceeds of crime.

• Ask for written confirmation of what the bank has done and any reports made to the financial intelligence authority or law enforcement.

A bank will normally ask you for a written explanation and may cooperate with law enforcement. Do not sign any document that admits fault or that authorises the bank to do anything other than investigate and preserve records until you have spoken to your lawyer. Guidance for reporting suspicious activity under the reporting framework urges both preservation of records and clear reporting by the reporting institution.

Practical steps to avoid appearing complicit

- Create an audit trail

Every step you take should be recorded. Save emails, text messages, and call logs. If you spoke to a bank officer, note the name, branch and time. - Do not alter or destroy evidence

Do not delete messages from the sender, do not wipe your phone, and do not remove any transaction messages. Destruction of evidence can itself trigger suspicion. - Return the funds only through proper channels

If the bank or the investigative authority confirms the credit is fraudulent, ask them to return it on your behalf or obtain written instruction on how to return it. Do not send the money back directly to an unknown account without confirming that that account belongs to the rightful owner or to the bank. - Be ready to explain legitimate reasons for the credit

If the money is a genuine gift, payment for work, or a mistaken transfer by someone you know, gather proof. This could be contracts, invoices, job messages, or correspondence that shows a legitimate basis for the transfer.

What to do if the police or investigators contact you

Cooperate but be cautious. Provide the documentary evidence you have preserved. If the police or an investigative agency request voluntary statements, ask for legal representation before giving the statement. An informed and calm response supported by contemporaneous records greatly reduces the risk that you will be mistaken for an accomplice.

Common scenarios and how to handle them

• A bank error or corporate refund

Notify the bank and ask them to correct the mistake. Keep copies of your communications.

• A family member or friend who sent the money by mistake

Ask the sender to confirm in writing that they sent the money by mistake and to instruct their bank to recall the transfer. Do not accept informal assurances by voice only.

• An apparent scam where you received proceeds of fraud

Contact your bank and provide them with all the evidence. Do not attempt to help the sender conceal the source of the funds.

Final practical checklist

- Do not spend the money.

- Screenshot and save everything.

- Contact your bank and request that the funds be placed on hold pending investigation.

- Get written confirmations for every instruction you give or receive.

- Speak to a lawyer and instruct them to request preservation of evidence from the bank.

- Avoid direct contact with unknown senders.

- Cooperate with official investigations and be ready to produce your preserved records.

Receiving an unexpected credit can be stressful. What protects you is timely, calm and recorded action. By preserving a clear record, notifying the bank, and involving legal advice if there is any doubt, you significantly reduce the chance that you will be treated as an accomplice rather than an innocent recipient. The law now has a strong focus on tracking and preventing money laundering. Acting immediately and transparently is the best safeguard. For statutory background on receiving stolen property and on the modern money laundering framework consult the relevant criminal code provision and the money laundering statute as updated.